Categories:

Key areas of focus

-

Labor market: The real focus this week will be Friday’s July Employment Situation report, with investors watching whether payroll growth, unemployment, hours worked, and wage growth confirm the Fed’s view that job gains remain broadly in line with labor-force growth.

-

Business activity: Monday’s ISM Manufacturing report and Wednesday’s ISM Services report will help determine whether the economy is still expanding at a solid pace, especially after Q2 GDP slowed to a 1.5% annualized rate while real final sales to private domestic purchasers accelerated to 3.9%.

-

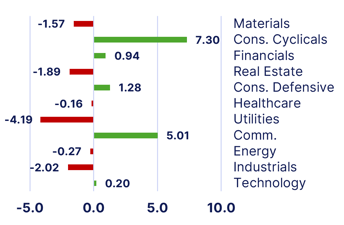

AI earnings and rates: Investors will continue to monitor whether strong cloud and AI-related earnings can offset pressure from higher long-term yields, with last week’s market gains led by Consumer Cyclicals and Communication Services while longer-term Treasury yields remained a key headwind.

Week in review

Markets finished the final week of July higher as investors balanced a busy macro calendar, another round of high-profile AI-related earnings (see “Spotlight” below), and a divided Federal Reserve. Monday began on a modestly constructive note, with durable goods orders rising 0.3% in June after a 4.0% decline in May. Tuesday brought a softer read on consumers, as The Conference Board Consumer Confidence Index slipped to 90.8 from an upwardly revised 92.2, while the Richmond Fed’s regional manufacturing data were mixed but still expansionary. Wednesday’s focus shifted to the Fed, which held the federal funds target range at 3.50% to 3.75% by a 9 to 3 vote, with three dissenters favoring a 25-basis-point hike. The split reinforced that inflation concerns remain unresolved, even as the Committee described economic activity as expanding at a solid pace. Thursday delivered the week’s most important macro data, with Q2 real GDP slowing to a 1.5% annualized rate from 2.1% in Q1. Personal Consumption Expenditures price inflation (the Fed’s preferred inflation measure) was mixed, with headline PCE prices falling 0.1% and core PCE prices (excluding food and energy) rising 0.1% in June from May.

Spotlight

The most important development last week was the market’s willingness to re-engage with the AI trade, but only where earnings offered clearer evidence that the spending cycle is translating into revenue. The prior week’s concern was that massive AI capital spending might not generate attractive returns quickly enough to justify elevated valuations. Last week’s earnings helped soften that concern, as Amazon and Microsoft shares surged after strong cloud-computing revenues, while Meta came under pressure as weaker-than-expected cash flow forced the company to defend elevated spending. The AI trade appears to be no longer simply about who is spending the most, but who can show the clearest path from investment to cash flow, revenue growth, and operating leverage. The stock prices of companies that can demonstrate tangible cloud demand, pricing power, and durable cash-flow benefits are being rewarded recently, while companies asking investors to underwrite large future spending without near-term evidence are facing more scrutiny.

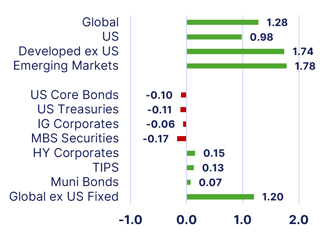

Markets

Sectors

Style & Market Cap

Sources

Durable Goods Orders: United States Census Bureau, Monthly Advance Report on Durable Goods Manufacturers’ Shipments, Inventories and Orders, retrieved from U.S. Census Bureau; Durable Goods Orders. https://www.census.gov/manufacturing/m3/adv/current/index.html

Consumer Confidence: The Conference Board, US Consumer Confidence, retrieved from The Conference Board; Consumer Confidence. https://www.conference-board.org/topics/consumer-confidence/index.cfm

Richmond Fed Manufacturing Index: Federal Reserve Bank of Richmond, Manufacturing Survey, retrieved from the Richmond Fed; Richmond Fed Manufacturing Survey. https://www.newyorkfed.org/medialibrary/media/markets/fomc-statement-20260729.pdf

Federal Reserve / FOMC Decision: Federal Reserve Bank of New York, Federal Reserve issues FOMC statement, July 29, 2026; FOMC Statement. https://www.newyorkfed.org/medialibrary/media/markets/fomc-statement-20260729.pdf

Gross Domestic Product: Bureau of Economic Analysis, GDP (Advance Estimate), 2nd Quarter 2026, retrieved from BEA; GDP Advance Estimate. https://www.bea.gov/news/2026/gdp-advance-estimate-2nd-quarter-2026

Personal Consumption Expenditures Price Index / Personal Income and Outlays: Bureau of Economic Analysis, Personal Income and Outlays, June 2026, retrieved from BEA; Personal Income and Outlays. https://www.bea.gov/news/2026/personal-income-and-outlays-june-2026

Market Data: Morningstar Direct using Morningstar Indices.

Author:

Nate Garrison

CFA®, CAIA®, CIPM®, FRM®

Chief Investment Officer

World Investment Advisors, LLC