Categories:

Key Takeaways:

- SpaceX is the largest IPO in financial history. SpaceX will list on the Nasdaq on June 12, 2026, at $135.00 per share, raising approximately $75 billion and implying a market capitalization of roughly $1.77 trillion. SpaceX will immediately be one of the top 10 largest public companies in the world. Only about 4.24% of total shares will be available for public trading at IPO, with a staggered lockup gradually increasing the float over six months. Despite generating $18.67 billion in revenue in 2025, SpaceX reported a GAAP net loss of -$4.94 billion.

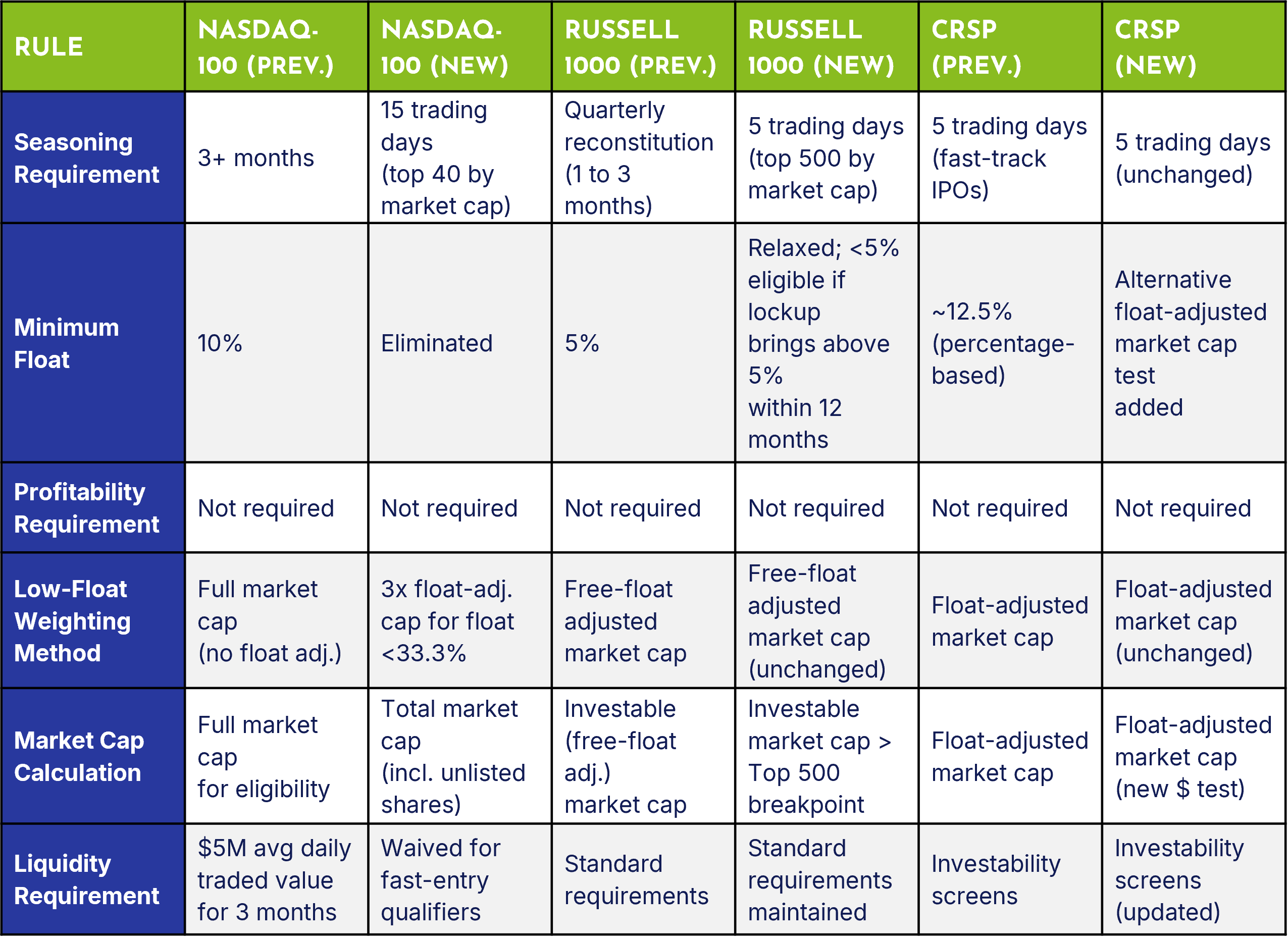

- Major index providers diverged sharply in their response to the IPO. Nasdaq, FTSE Russell, and CRSP (Morningstar) all adopted "Fast Entry" rules allowing inclusion in the Nasdaq-100 (after 15 trading days), the Russell 1000 (after 5 trading days), and the CRSP US Total Market Index (after 5 trading days), while relaxing or eliminating prior minimum float requirements; none of these indexes requires profitability. In contrast, S&P Dow Jones Indices announced on June 4, 2026, that it would maintain the S&P 500's existing 12-month seasoning period, GAAP profitability requirement, and 10% minimum float threshold. SpaceX will not be eligible for S&P 500 inclusion until at least June 2027.

- The index rule changes carry both positive and negative implications for passive index fund investors. Faster inclusion in the Nasdaq-100, Russell 1000, and CRSP indexes improves market representativeness. However, index funds will be compelled to purchase SpaceX shares after as few as 5 to 15 trading days of price history, and mechanical buying pressure into a stock with only 4.24% float could amplify volatility. S&P's decision protects S&P 500 index fund investors from premature forced buying, but those investors risk missing potential upside if SpaceX appreciates before its eventual inclusion.

- Investors in different large-cap U.S. equity index funds will have very different SpaceX exposure. SpaceX's estimated Nasdaq-100 weight could reach approximately 4.88% as the float expands, while its Russell 1000 weight may grow from approximately 0.12% at inclusion to approximately 2.87% at full float. Its S&P 500 weight will remain zero until inclusion in June 2027 at the earliest. Collectively, the indexes discussed in this bulletin have over $20 trillion in benchmarked assets, making these differences consequential for a very large number of investors.

- The SpaceX IPO underscores the importance of understanding the index behind the fund. The S&P 500 applies a profitability screen and committee selection process; the Russell 1000, Nasdaq-100, and CRSP indexes do not. The inclusion of SpaceX (an unprofitable company) in these indexes but not the S&P 500 widens the quality gap and may increase tracking error between benchmarks for 12 months or longer. When selecting an index fund, investors and fiduciaries should evaluate the index's eligibility rules, weighting methodology, and quality criteria.

- The index rule changes may establish a new path for private equity and venture capital exits. By enabling rapid index inclusion for large IPOs with very low floats and no profitability requirement, the new rules create a pathway for PE and VC-backed companies to go public and immediately benefit from passive buying pressure. This could expand the public investable universe by encouraging more companies to list sooner, but it also risks making passive index fund investors (including retirement plan participants) the exit liquidity for early-stage sponsors.

History in the Making

Space Exploration Technologies Corp. (SpaceX) will list its Class A common stock on the Nasdaq Global Select Market under the ticker symbol SPCX on Friday, June 12, 2026. This offering from the space/satellite communications/artificial intelligence/social media company is poised to become the largest initial public offering (IPO) in financial history. This single company will raise more capital in one morning than most S&P 500 companies are worth in their entirety. At a $1.77 trillion valuation, SpaceX would immediately be worth more than all but the ten largest publicly traded companies in the world.

For investors in passive index funds, the SpaceX initial public offering also carries implications that extend well beyond the company itself. The way major index providers have responded to this listing affects how and when SpaceX enters the benchmarks that drive trillions of dollars in passive investment capital.

This Market Bulletin provides an overview of the index rule changes (and non-changes) that will shape its path into major benchmarks, and what these developments mean for investors in US equity index funds.

IPO Overview

SpaceX has set a fixed offering price of $135.00 per share for its IPO. The company plans to sell 555,555,555 Class A shares, raising approximately $75 billion in gross proceeds. Elon Musk will retain over 82% voting control through his ownership of Class B shares with super-voting rights.

At the $135-per-share IPO price, SpaceX would carry an implied market capitalization of approximately $1.77 trillion, making it roughly the seventh-largest publicly traded company in the United States (ahead of Tesla, which had a market capitalization of approximately $1.6 trillion at the time of filing). The $75 billion raise would shatter the previous record for a single IPO, more than doubling Saudi Aramco's $29.4 billion offering in 2019 and roughly tripling Alibaba's $25 billion U.S. IPO in 2014.

Although SpaceX generates many headlines, it does not currently generate any accounting profits. SpaceX reported a GAAP net loss of $4.94 billion for the 2025 fiscal year, driven primarily by capital expenditures and operating losses in the AI segment. The company reported a $4.28 billion net loss in Q1 2026 alone. (Notably, SpaceX’s AI segment exists because SpaceX merged with xAI in February 2026 and retroactively recast its financials, resulting in a loss. The core space and satellite communications businesses were profitable before the merger, with Starlink alone generating $4.4B in operating income in 2025.)

From IPO to Index Constituent

In anticipation of the SpaceX IPO (and other large expected listings such as OpenAI and Anthropic), both Nasdaq Global Indexes and FTSE Russell made significant changes to their index inclusion methodologies in early 2026. These changes directly affect how quickly SpaceX will enter the Nasdaq-100 Index and the Russell 1000 Index (including the Russell 1000 Growth Index), and at what weighting.

Nasdaq-100 Index Changes (Effective May 1, 2026)

The Nasdaq-100 is one of the most widely followed equity indexes in the world, with approximately $652 billion in ETF assets directly tracking the index (including the Invesco QQQ Trust at approximately $496 billion and the Invesco Nasdaq 100 ETF at approximately $99 billion), plus additional mutual fund and institutional assets.

Following a formal public consultation, Nasdaq Global Indexes implemented targeted updates to the Nasdaq-100 methodology effective May 1, 2026. The most consequential change is a new "Fast Entry" provision that allows a newly listed company to enter the Nasdaq-100 after just 15 trading days if its total market capitalization ranks within the top 40 current Nasdaq-100 constituents (a threshold of approximately $100 billion as of year-end 2025). Under the previous rules, a newly listed stock was required to season for at least three months before it could be considered for inclusion.

In addition, the previous minimum 10% free float requirement has been eliminated entirely. To address the risk of disproportionate index weight relative to tradable shares, Nasdaq introduced a low-float weighting adjustment: for companies with a free float below 33.3%, the index weight is calculated at 3 times the float-adjusted market capitalization (rather than the full market capitalization that was previously used).

A fast-entry addition does not require the removal of another security from the Nasdaq-100; the index can temporarily expand beyond 100 constituents until the next annual reconstitution in December.

FTSE Russell Index Changes (Effective May 26, 2026)

The Russell US Indexes (including the Russell 1000 and Russell 1000 Growth) had approximately $12.2 trillion in benchmarked assets as of June 2025, according to FTSE Russell, making them among the most widely used equity benchmarks in the world.

FTSE Russell, following a market consultation conducted in February 2026, approved a new Fast Entry mechanism for its Russell U.S. Equity Indexes. Under the new rule, IPOs are eligible for index inclusion after just five days of public trading if they have an investable market capitalization exceeding the market-adjusted total market capitalization breakpoint for the Russell Top 500 (approximately $17.5 billion as of the current cycle). Under the previous rules, IPOs were reviewed only at quarterly reconstitution dates, meaning newly listed companies could wait one to three months for inclusion.

FTSE Russell also relaxed its minimum 5% free float and 5% public voting rights requirements for qualifying IPOs. Companies with less than 5% float or voting rights at IPO will be considered eligible if their lockup arrangements are expected to bring the company above those minimums within 12 months of index inclusion. SpaceX's staggered lockup schedule, as outlined in its S-1 filing, appears designed to satisfy this condition.

Importantly, the Russell indexes continue to use free-float adjusted market capitalization for weighting purposes (they do not apply a multiplier like the Nasdaq-100).

CRSP Market Indexes Changes (Effective April 27, 2026)

The CRSP US Total Market Index (maintained by the Center for Research in Security Prices, now part of Morningstar) serves as the benchmark for several of the largest index funds in the world, including the Vanguard Total Stock Market ETF (VTI, approximately $660 billion in assets) and the Vanguard Total Stock Market Index Fund (VTSAX). The CRSP Large Cap Growth Index underpins the Vanguard Growth ETF (VUG). In total, well over $1.5 trillion in fund assets track CRSP U.S. equity indexes.

Since 2017, CRSP Market Indexes have included eligible IPOs on the fifth trading day after listing, a fast-track mechanism that was already faster than Nasdaq's previous three-month requirement and Russell's previous quarterly review cycle. However, under the previous methodology, IPOs with a public float below approximately 12.5% of total shares outstanding were excluded by CRSP's Float Shares Investability Screen, regardless of the absolute size of the float.

On February 25, 2026, CRSP announced a change to its Float Shares Investability Screen. Effective April 27, 2026, CRSP added an alternative float-adjusted market capitalization test, allowing large companies to qualify for index inclusion even when their float percentage falls below the traditional threshold, as long as their absolute float-adjusted market capitalization meets a minimum dollar value. This change was explicitly designed to address the new reality of mega-IPOs from companies that have remained private longer, resulting in larger, more mature firms at IPO with lower float percentages but substantial absolute dollar float values.

Like the Russell indexes, CRSP uses float-adjusted market capitalization for weighting purposes. It does not apply a multiplier (as the Nasdaq-100 does). As a result, SpaceX's initial weight in CRSP-based funds like VTI will be modest (reflecting only the 4.24% float) and will grow over time as lockup releases increase the tradable share count. In its May 2026 research paper, Morningstar noted that "the expiration of a lockup period after IPO will have a greater impact on the indexes and index funds than mega-IPOs' initial inclusion in the index."

Summary of Key Rule Changes: Nasdaq-100, Russell 1000, and CRSP

Estimated SpaceX Index Weights Over Time

The table below presents our estimates of SpaceX's expected index weight in the Nasdaq-100, Russell 1000, and Russell 1000 Growth indexes at key dates, assuming constant market values for SpaceX and all other index constituents. For these estimates, we used an approximate total market capitalization of $34.5 trillion for the Nasdaq-100 (as of end of May 2026), an estimated free-float adjusted total market capitalization of approximately $60 trillion for the Russell 1000, and approximately $35 trillion for the Russell 1000 Growth. SpaceX's weight in CRSP-based funds (such as VTI) would be similar to, but slightly smaller than, its Russell 1000 weight, given the broader universe of the CRSP US Total Market Index.

Note: Actual weights will vary based on changes in SpaceX's stock price, changes in the market values of other index constituents, and the specific timing of lockup releases and index rebalancing events. All weight estimates assume constant market values. Nasdaq-100 weights reflect the 3x low-float multiplier for float below 33.3%; once float exceeds 33.3% (approximately Day 135), SpaceX transitions to full market cap weighting in the Nasdaq-100 (capped at approximately 4.88% given the current Nasdaq-100 composition). Russell 1000 weights are based on free-float adjusted market capitalization. Elon Musk's shares (~42% of total equity) remain locked until approximately June 2027; full float (100%) would imply an estimated Russell 1000 weight of ~2.87% and a Russell 1000 Growth weight of ~4.81%.

Note: Actual weights will vary based on changes in SpaceX's stock price, changes in the market values of other index constituents, and the specific timing of lockup releases and index rebalancing events. All weight estimates assume constant market values. Nasdaq-100 weights reflect the 3x low-float multiplier for float below 33.3%; once float exceeds 33.3% (approximately Day 135), SpaceX transitions to full market cap weighting in the Nasdaq-100 (capped at approximately 4.88% given the current Nasdaq-100 composition). Russell 1000 weights are based on free-float adjusted market capitalization. Elon Musk's shares (~42% of total equity) remain locked until approximately June 2027; full float (100%) would imply an estimated Russell 1000 weight of ~2.87% and a Russell 1000 Growth weight of ~4.81%.

S&P 500 to Maintain Existing Index Rules

The S&P 500 is the most widely followed equity benchmark in the world. Passive S&P 500 index funds and ETFs hold trillions of dollars in assets. The Vanguard S&P 500 ETF (VOO) recently became the first ETF in history to surpass $1 trillion in assets under management (as of June 3, 2026). Together with the iShares Core S&P 500 ETF (IVV, approximately $860 billion) and the SPDR S&P 500 ETF Trust (SPY, approximately $786 billion), the three largest S&P 500 ETFs alone hold over $2.6 trillion. Including mutual funds and institutional mandates, total assets indexed to the S&P 500 are estimated at over $7.5 trillion.

On June 4, 2026, S&P Dow Jones Indices (S&P DJI) announced the results of its market consultation on the treatment of mega-cap companies. In contrast to Nasdaq and FTSE Russell, S&P DJI determined that no changes would be made to the eligibility criteria for the S&P 500, S&P MidCap 400, or S&P SmallCap 600.

In its press release, S&P DJI stated: "Exceptions to the financial viability, seasoning, and IWF requirements should not be granted solely based on market capitalization. The decision not to adopt the proposed exceptions preserves core index principles by maintaining consistent application of these key requirements."

Current S&P 500 Eligibility Requirements (Unchanged)

S&P Dow Jones Indices' Rationale

S&P Dow Jones Indices' Rationale

S&P DJI had consulted with market participants about several potential changes, including shortening the 12-month seasoning period to 6 months for mega-cap IPOs, waiving the profitability requirement for companies exceeding a certain market capitalization threshold, and relaxing the minimum IWF requirement.

After reviewing all consultation responses, S&P DJI concluded that "although there may be trade-offs between strict adherence to these eligibility requirements and broad representativeness, the current methodology provides substantial market coverage and sector balance. As a result, the indices can continue to meet their stated objectives while preserving their role as representative and investable benchmarks for the U.S. equity market."

For SpaceX specifically, the decision means the company will not be eligible for S&P 500 inclusion until at least June 2027 (12 months after listing), and only if it satisfies the profitability requirement at that time. Given that SpaceX reported a $4.94 billion GAAP net loss in 2025 and a $4.28 billion net loss in Q1 2026 alone, meeting the four-quarter profitability requirement may take longer.

Implications for Current Nasdaq, Russell and CRSP Index Fund Investors

The rule changes adopted by Nasdaq, FTSE Russell, and CRSP have both positive and negative implications for investors owning the trillions of dollars invested in passive funds tracking their indexes.

Positive Implications

Improved Market Representativeness: Index funds aim to provide investors with exposure to the investable equity market. Excluding a company with a $1.77 trillion market capitalization from major benchmarks for months (or years) creates a gap between the index and the actual market. Faster inclusion ensures that index fund investors have exposure to economically significant companies sooner, reducing the risk of underperformance relative to the broader market.

Reduced Tracking Error for Total Market Strategies: For investors using index funds as building blocks in diversified portfolios, the absence of major companies from their benchmarks can introduce unintended tracking error relative to the total market. Faster inclusion reduces this gap.

Gradual Float Expansion May Reduce Lockup Disruption: SpaceX's staggered lockup structure, combined with the Nasdaq-100's 3x low-float weighting multiplier and the Russell and CRSP indexes' free-float adjusted weighting, means that SpaceX's index weight will grow gradually as more shares become available for trading. This phased approach may reduce the disruptive impact of a single large lockup expiration event.

Negative Implications and Risks

Forced Buying into a Low-Float, Newly Public Stock: Index funds tracking the Nasdaq-100 (approximately $652 billion in ETF assets), the Russell 1000 (approximately $12.2 trillion in benchmarked assets across all Russell US Indexes), and CRSP indexes (over $1.5 trillion in fund assets) will be required to purchase SpaceX shares regardless of the company's fundamentals, valuation, or trading history. With only approximately 4.24% of shares available for public trading at IPO, the mechanical buying pressure from passive funds could amplify price volatility and contribute to an inflated entry price for index fund investors.

Limited Price Discovery Period: Fifteen trading days (for the Nasdaq-100) and five trading days (for the Russell 1000 and CRSP indexes) provide very little time for the market to establish reliable pricing for a newly public stock. Index fund investors are effectively required to buy at whatever price the market sets during this compressed window.

Precedent for Future Low-Float, High-Valuation IPOs: The rule changes create a template for other large private companies to go public with very low floats and gain rapid index inclusion, effectively compelling passive capital to provide exit liquidity for early-stage investors. This dynamic is discussed later in this Market Bulletin.

Implications for Current S&P 500 Index Fund Investors

S&P Dow Jones Indices' decision to maintain its existing eligibility criteria has distinct implications for investors in S&P 500 index funds (including widely held funds and ETFs such as the Vanguard 500 Index Fund, the Fidelity 500 Index Fund, the SPDR S&P 500 ETF, and the iShares Core S&P 500 ETF).

Positive Implications

Protection from Premature Forced Buying. S&P 500 index fund investors will not be required to purchase SpaceX shares until the company has traded publicly for at least 12 months and demonstrated GAAP profitability. This protects investors from the risks associated with buying into a low-float, newly public stock at potentially inflated prices. Bloomberg Intelligence estimated that fast inclusion would have triggered approximately $14 billion in forced passive buying for SpaceX; that buying will now be delayed until at least a year after the IPO.

Preservation of Index Quality Standards. The S&P 500's profitability requirement serves as a quality screen that distinguishes it from the Russell 1000 and Nasdaq-100. By maintaining this requirement, S&P DJI preserves the index's historical character as a benchmark of profitable, established U.S. large-cap companies. This is particularly relevant for fiduciaries who must select investment options that are prudent and in the best interests of clients and plan participants.

Negative Implications and Risks

Potential Missed Upside. If SpaceX's stock price appreciates significantly in the months following its IPO, S&P 500 index fund investors will not participate in those gains until the company is added to the index. This is the same dynamic that occurred with Tesla, which traded publicly for over 10 years before joining the S&P 500 in December 2020.

Divergence from Other Major Benchmarks. The S&P 500 will now diverge from the Russell 1000 and Nasdaq-100 in its treatment of SpaceX. This creates a period of meaningful compositional difference between these benchmarks, which has implications for tracking error and relative performance. This is discussed further below.

Implications for Selecting Index Funds

Diverging Index Philosophies

The SpaceX IPO has exposed a fundamental philosophical divide among the three major U.S. equity index providers. Nasdaq and FTSE Russell have prioritized representativeness (ensuring their indexes reflect the largest companies in the market as quickly as possible), while S&P Dow Jones has prioritized quality and stability (maintaining profitability, seasoning, and float requirements that have historically served as guardrails for passive investors). Neither approach is inherently right or wrong; each involves trade-offs that investors should understand.

Key Impacts of Compositional Divergence

A single stock with a market capitalization exceeding $1.7 trillion will be a constituent of the Russell 1000, Nasdaq-100, and CRSP Total Market indexes, but absent from the S&P 500. This creates several notable dynamics for index fund investors. For investors and fiduciaries evaluating large-cap U.S. equity index fund options, the distinction between the underlying index is now more consequential than it has been in recent years.

Increased Tracking Error Between the S&P 500 and Russell 1000. The inclusion of SpaceX in the Russell 1000 but not the S&P 500 will introduce a source of tracking error between these two benchmarks that could persist for 12 months or longer. If SpaceX performs well, the Russell 1000 will outperform the S&P 500 (all else equal); if SpaceX performs poorly, the reverse will occur. This is an important consideration for investors and fiduciaries who may use one of these indexes as a benchmark to evaluate the performance of a fund or a portfolio.

Differences in Underlying Index Quality. The S&P 500 applies a profitability screen and a committee selection process; the Russell 1000, Nasdaq-100, and CRSP indexes do not. As a result, the S&P 500 has historically maintained a higher average quality profile among its constituents (in terms of earnings consistency and financial stability) compared to the Russell 1000, which is purely rules-based and includes all qualifying large-cap companies regardless of profitability. The inclusion of SpaceX (a company with a $4.94 billion net loss) in the Russell 1000 but not the S&P 500 widens this quality gap.

Concentration and Weighting Differences. In the Nasdaq-100, SpaceX's weight could reach approximately 4.88% at full float (given the 3x low-float multiplier transitioning to full market cap weighting). In the Russell 1000, SpaceX's weight would start at approximately 0.12% and could grow to approximately 2.87% at full float. In CRSP-based funds, the weight would be similar to but slightly smaller than the Russell 1000. In the S&P 500, SpaceX's weight will be zero until inclusion (at least June 2027). These weighting differences mean that investors in funds tracking different indexes will have different exposure to SpaceX, even if they believe they hold "similar" large-cap U.S. equity funds.

The Importance of Understanding the Underlying Index

The SpaceX IPO serves as an important reminder that not all large-cap U.S. equity index funds are the same. When selecting an index fund for a client portfolio, a retirement plan investment lineup, or a personal investment account, it is essential to understand the rules of the underlying index that the fund tracks.

Key questions to consider include:

- What are the index's eligibility requirements (including seasoning, profitability, and float thresholds)?

- How does the index weight its constituents (full market cap vs. free-float adjusted)?

- How quickly does the index add newly public companies?

- Does the index apply any quality or financial viability screens?

The answers to these questions can lead to meaningfully different portfolio compositions, risk exposures, and performance outcomes, even among funds that are commonly perceived as interchangeable.

Broader Implications: A New Path for Private Equity Exits?

Beyond SpaceX, the index rule changes adopted by Nasdaq, FTSE Russell, and CRSP may have broader implications for the relationship between private markets and public markets. The new rules do not just open the door for SpaceX; they open it for every large private company behind it.

By creating a pathway for large, newly public companies to enter major benchmarks within days or weeks of their IPO (even with very low floats and no profitability requirement), these rule changes effectively create a new exit mechanism for private equity (PE) and venture capital (VC) firms. This dynamic has both potential benefits and risks for investors in passive index funds.

Potential Benefits

Faster index inclusion may encourage more large private companies to go public, which could expand the investable universe for index fund investors and reduce the growing gap between private and public market opportunity sets. Companies like OpenAI, Anthropic, and others in the pipeline may bring innovative businesses to public markets sooner, giving retirement plan participants and individual investors access to growth opportunities that were previously available only to institutional and accredited investors in private markets.

Potential Risks

The same dynamic could also create a situation in which passive index funds effectively serve as exit liquidity for PE and VC sponsors. In this scenario, the sponsors exit at high valuations while the ongoing risk is transferred to passive investors (including retirement plan participants) who have no choice but to hold the stock as long as it remains in the index. If the company underperforms after its IPO, passive investors bear the loss, while early sponsors have already realized their gains. This concern is amplified when the company entering the index is unprofitable and has a very thin public float, as the price discovery process may be distorted by the imbalance between limited supply and mechanically driven demand.

What next?

Investors should remain attentive to these structural changes in the index landscape. Not all large-cap U.S. equity index funds are the same, and after June 12, the differences will be harder to ignore.

The index your passive fund tracks is an investment decision, whether you realize it or not. Therefore, understanding the index behind the passive fund is a fundamental component of prudent investment selection.

To help with this process, the WIA Investment Team will publish additional research and resources to aid investors and advisors in selecting index funds in the coming months. In the meantime, please feel free to contact us with any questions about index funds or other investment topics.

Disclosures:

This Market Bulletin is provided for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any security. The information contained herein is based on publicly available sources believed to be reliable as of the date of publication; however, World Investment Advisors makes no representation or warranty as to its accuracy or completeness. Index weight estimates presented in this bulletin are forward-looking calculations based on assumptions described herein (including constant market values) and are subject to change based on actual market conditions, index provider decisions, and the specific timing of lockup releases and rebalancing events. Errors may exist within this document. Past performance is not indicative of future results. Investors should consult with their financial advisor before making any investment decisions.

Sources:

Bloomberg. (2026, June 4). SpaceX, other mega IPOs denied fast index entry by S&P. Bloomberg News. https://www.bloomberg.com/news/articles/2026-06-04/s-p-dow-jones-keeps-megacap-ipo-rules-as-is-after-consultation

CNBC. (2026, May 21). SpaceX insiders will get to sell shares earlier than usual after the IPO. https://www.cnbc.com/2026/05/21/spacex-insiders-will-get-to-sell-shares-earlier-than-usual-after-the-ipo.html

CNBC. (2026, June 3). SpaceX targets $135 IPO price at valuation of $1.77 trillion. https://www.cnbc.com/2026/06/03/spacex-ipo-stock-price-roadshow-musk.html

CNBC. (2026, June 4). SpaceX blocked from early U.S. benchmark index entry as S&P reaffirms existing rules. https://www.cnbc.com/2026/06/05/spacex-blocked-from-early-us-benchmark-index-entry-as-sp-reaffirms-existing-rules.html

CRSP (Center for Research in Security Prices). (2026, February 25). CRSP Market Indexes notification: Changes to Float Shares Investability Screen. https://www.crsp.org/

CRSP (Center for Research in Security Prices). (2026, April 27). April 2026 CRSP Market Indexes Methodology Guide updates. https://www.crsp.org/april-2026-crsp-market-indexes-methodology-guide-updates/

ETF Stream. (2026, May 27). FTSE Russell indexes to fast-track entry of US mega-IPOs. https://www.etfstream.com/articles/ftse-russell-indexes-to-fast-track-entry-of-us-mega-ipos

Forbes. (2026, April 25). SpaceX IPO is forcing changes to index and underwriting rules. https://www.forbes.com/sites/garthfriesen/2026/04/25/spacex-ipo-is-forcing-changes-to-index-and-underwriting-rules/

Forbes. (2026, June 4). Ordinary people can invest in SpaceX IPO: Here's how and why it's risky. https://www.forbes.com/sites/tylerroush/2026/06/04/ordinary-people-can-invest-in-spacex-ipo-heres-how-and-why-its-risky/

FTSE Russell. (2026, February). Market consultation: Consultation for the Russell US Equity Indexes on the timing of IPOs and the treatment of companies with a high free float market capitalization. https://www.lseg.com/content/dam/ftse-russell/en_us/documents/consultation/ipo-fast-entry-consultation.pdf

FTSE Russell. (2026, May 22). FTSE Russell begins June 2026 semi-annual Russell US Indexes reconstitution [Press release]. https://www.lseg.com/en/media-centre/press-releases/ftse-russell/2026/ftse-russell-begins-june-2026-semi-annual-russell-us-indexes-reconstitution

FTSE Russell. (2026, May 26). Market consultation: Russell US Equity Indexes IPO fast entry and minimum eligibility requirements [Index notice]. https://research.ftserussell.com/products/index-notices/home/getmethodology?id=2619701

FTSE Russell. (2026, April 10). Russell reconstitution 2026 is approaching: Here's what you need to know. https://www.lseg.com/en/insights/ftse-russell/russell-reconstitution-2026-is-approaching-heres-what-you-need-to-know

InvestmentNews. (2026, May 28). SpaceX's index fund debut will look nothing like what most investors expect, says Jacob Friedman. https://www.investmentnews.com/practice-management/spacexs-index-fund-debut-will-look-nothing-like-what-most-investors-expect-says-jacob-friedman/266776

Investopedia. (2026, June 5). The SpaceX IPO will ripple across indexes and funds. Here's what that means and doesn't mean. https://www.investopedia.com/the-spacex-ipo-will-ripple-across-indexes-and-funds-here-s-what-that-means-and-doesn-t-mean-11992004

Morningstar. (2026, April 8). The SpaceX IPO: How index funds will adapt. https://www.morningstar.com/funds/spacex-ipo-how-index-funds-will-adapt

Nasdaq Global Indexes. (2026, May). Nasdaq-100 Index methodology changes: Frequently asked questions. https://indexes.nasdaqomx.com/docs/2026_May_NDX_Changes_FAQ.pdf

Nasdaq. (2026, May 8). Nasdaq-100 Index methodology update: Why now, and what it means. https://www.nasdaq.com/newsroom/nasdaq100-index-methodology-update-why-now

Reuters. (2026, June 4). SpaceX blocked from early US benchmark index entry as S&P reaffirms existing rules. https://www.reuters.com/business/finance/sp-global-keeps-fast-entry-proposal-unchanged-spacex-listing-looms-2026-06-04/

S&P Dow Jones Indices. (2026, June 4). S&P Dow Jones Indices consultation results on MegaCap company treatment [Press release]. As reported by Traders Magazine. https://www.tradersmagazine.com/xtra/sp-does-not-change-megacap-eligibility-for-indices/

Space Exploration Technologies Corp. (2026, May 20). Form S-1 Registration Statement. U.S. Securities and Exchange Commission. CIK 0001181412.

Space Exploration Technologies Corp. (2026, June 3). Form S-1/A Amendment No. 1. U.S. Securities and Exchange Commission.

State Street Global Advisors. (2026, April 22). Mega-cap IPOs: Implications for institutional investors and index managers. https://www.ssga.com/us/en/institutional/insights/mega-cap-ipos-implications-for-institutional-investors-and-index-managers

Yahoo Finance. (2026, June 5). SpaceX confirms it will seek $75 billion in record IPO. https://finance.yahoo.com/markets/stocks/article/spacex-launches-ipo-website-for-retail-investors-as-it-seeks-record-75-billion-in-public-offering-next-week-213415729.html

Authors:

Nate Garrison

CFA®,CAIA,CIPM,FRM

Senior Vice President/Chief Investment Officer

World Investment Advisors, LLC

Anthony Silva

CFA®

Senior Director of Strategy Management

World Investment Advisors, LLC