Categories:

RECAP: WHAT HAPPENED LAST WEEK?

US President Donald Trump announced a slate of tariffs on the United States’ trading partners after the market closed on Wednesday April 2, ranging from a minimum of 10% to a high of 50%. These tariffs apply to most imported goods, except for certain key imports including semiconductors, pharmaceuticals, copper, and lumber. The tariff rates on some of its largest trading partners included 34% on China, 32% on Taiwan, 25% on South Korea, 24% on Japan, and 20% on the European Union. Most goods from Mexico and Canada that comply with the US- Mexico-Canada Agreement (“USMCA”) will remain mostly exempt from the new round of tariffs. Collectively, these are the highest tariff rates the United States has implemented in many decades.

Subsequently, China announced plans to impose retaliatory tariffs of 34% on United States exports to their country, starting April 10. Canada announced an import tariff of 25% on vehicles imported from the United States. The European Union is similarly exploring a response to the new US tariffs on their goods. Several countries have also announced they would like to work with the administration to lower their new tariff rate.

US stocks were mostly positive for the week going into the April 2 announcement, with the S&P 500 Index up ~1.6% from Friday March 28’s close through the close on April 2. That quickly changed when a “risk-off” trade enveloped markets around the world, with equities and other riskier assets being sold in favor of safe haven assets like cash and US Treasuries. Market participants were expecting an increase in tariffs, but the actual level of the rates took many by surprise. US equities, which have been richly valued relative to other asset classes, suffered some of the worst losses, as investors fled them in droves on Thursday April 3 and again on Friday April 4. The S&P 500 finished the week down over -9%, its worst weekly performance since the height of the COVID Pandemic in March 2020.1

TRUMP’S TARIFFS AS POLICY TOOLS

Tariffs have been used as a policy tool since the birth of the United States almost 250 years ago. Over the past 80 years since the end of World War II US presidents have generally worked to lower trade barriers and tariffs around the world. The Trump administration is making a break with this recent past.

Trade economist Douglas Irwin highlights in his book “Clashing Over Commerce: A History of US Trade Policy” that tariffs have generally been used by the US government for one or more of three purposes, which he labels as the “Three Rs”:

- Revenue: Raising funds for government spending (i.e., a tax);

- Restrictions: Protecting certain domestic industries from foreign competition;

- Reciprocity: Pursuing agreements with other countries to open foreign markets to more US exports.

In many respects, the Trump administration is seeking to use tariffs as a policy tool for all of these “Three Rs”2

Revenues

The tariffs act as a consumption tax on imported goods and services. The Tax Foundation estimates that the new tariffs will generate an additional $258.4 billion in government revenue in 2025, which averages out to around $1,900 per US household. The Tax Foundation expects the new tariffs to raise $1.5 trillion in revenue over the next decade. This is in addition to previously announced tariffs, which the Tax Foundation estimates will raise $1.3 trillion in revenue over the next decade, for a total of $2.9 trillion over 10 years. These estimates also account for the Tax Foundation’s estimates of reduced imports as a result of the higher prices caused by the tariffs.3

A less broadcasted goal of the tariffs is to reduce interest rates. Administration officials have stated multiple times their desire to lower interest rates, including the key 10-year US Treasury rate.4 This comes in advance of waves of massive refinancing of government debts from years of deficit spending and the COVID Pandemic-era stimulus. Slower economic activity and lower GDP growth due to tariffs can contribute to lower interest rates, which can reduce the costs of borrowing.

Restrictions

One of the key goals of the administration’s tariff policy is to encourage companies to “onshore” or “reshore” production activities in the United States, which would be exempt from tariffs. The administration believes goods produced in the United States will now be priced competitively with similar goods produced in places like China or the European Union, which are subject to the tariffs. They believe this will cause a manufacturing boom in the United States, by protecting US manufacturers from foreign competition and, by extension, increasing US manufacturing jobs.

Reciprocity

The Trump administration has labeled the new tariffs as “reciprocal tariffs”, which are intended to counter the tariffs charged on goods exported by the United States. This characterization is debatable, as the new tariffs are instead based on bilateral trade deficits rather than actual tariff rates and fees levied by trading partners. In any case, the administration believes that the new tariffs will encourage trading partners to negotiate new trade arrangements that the administration finds more preferential to the United States.

IMPACTS ON THE US ECONOMY

The new tariffs are a tax on imported goods. Their impact will be similar to a tax increase. All else being equal, tax increases take money out of the economy and slow down economic activity. The impacts include lower job creation, higher prices, and reduced consumer spending. It is too early to predict the full extent of these impacts. However, the risk of recession is much more elevated than before the new tariffs.

We note that the US economy has been doing well over the past several years. The Federal Reserve, tasked with its dual mandate of maintaining full employment and price stability, sought a “soft landing” of reducing post-COVID inflation without crashing the labor market. It has been successful in its goal so far, with annualized inflation rates dropping from north of 9% to below 3% (though still above the Fed’s 2% long-term target) and unemployment hovering around 4% for many months in a row through the first quarter of this year.

Fed Chair Jerome Powell noted in a speech on Friday, April 4, 2025, “Looking ahead, higher tariffs will be working their way through our economy and are likely to raise inflation in coming quarters … [and while] tariffs are highly likely to generate at least a temporary rise in inflation, it is also possible that the effects could be more persistent.”5

Powell’s comments during the question-and-answer session after his Friday speech suggest that the Fed will continue to monitor economic conditions, but they will not act (i.e., cut the Fed Funds Rate) until they have more clarity on the trajectory of inflation or labor markets.

President Trump urged the Fed to cut rates immediately, citing lower inflation and falling energy prices.6 Jobs data released Friday, April 4, reported that 228,000 jobs were added, and the unemployment rate remains near full employment at 4.2% nationally.7 This helps make the case for the Fed that immediate rate cuts are not needed (yet).

IMPACTS ON MARKETS

Fixed Income

Although the Fed is holding firm for now, market participants are anticipating lower rates in the coming years. The yield curve has seen rates drop over 20bps between the 1- to 10-year Treasuries from immediately prior to the tariff announcements through Friday’s market close. The 2-year Treasury is now at its lowest rate since 2022.

US Treasury Yield Curve

IMPACTS ON MARKETS (CONTINUED)

Treasury yields have also been impacted by a “flight to safety”, as concerns grow about the risk of a recession in the United States sparked by the tariffs. For similar reasons, riskier credits saw their spreads over Treasuries expand; the ICE BofA US High Yield Index Option-Adjusted Spread increase by 59 bps (!) on Thursday alone, from 3.42 to 4.01 (widening spreads typically result in relative underperformance).8 This was the largest daily widening in high yield spreads since March 2020, and one of the top 20 largest daily widenings in spreads since 1996.

However, most fixed income (excluding High Yield) ended positive for the week, and remained positive for the year-to- date period and last 1-year trailing time period through April 4, 20259:

Equities

Equity indexes around the globe were crushed on Thursday and Friday on expectations of slower economic growth and reduced corporate profits due to tariffs. US stocks suffered far worse than their international peers, as the rich valuations of US stocks contracted on expectations that profit growth will likely be lower across the board with the costs of the new tariffs.

We note that US equities overall are basically where they were one year ago, and international equities are still up over the past 1-year period.10 As we noted in our earlier Market Bulletin from Thursday, March 13, 2025, drawdowns are common in equity markets over time, but the velocity of this drawdown is severe.

LOOKING AHEAD

Recent market movements are concerning, especially the speed at which the markets moved downwards. The new tariffs present economies with new, real costs, and the full extent of their impact is unclear. We note a few things for investors to consider as we look ahead:

Nearer Term:

Market volatility may remain high.

Stocks may continue to be very volatile. There may be more days of sharp declines, followed by days of markets ripping upwards. As the economy undergoes a transformation brought on by the tariffs, this will create frictions and increase uncertainty. When uncertainty is elevated and rising, valuations tend to suffer. We expect market participants will likely be very active in trading and reallocating their portfolios until we reach a “new normal” with more clarity on the future trajectory of the global economy many months from now.

US equities remain richly valued relative to international peers.11

US equities are more richly valued versus international equities. One can argue that the valuation differential is well deserved, given the strong relative performance of the US economy and US businesses in recent years.

Relative TTM P/E Ratios: US Equities vs Global Ex US Equities

LOOKING AHEAD (CONTINUED)

However, multiple contraction is a real (and recently realized) risk. If market participants become increasingly unsure of the direction of the US economy or economic policy, they may require a higher risk premium (through a lower valuation) to own US stocks. If that comes to pass, then US equities may be downwardly pressured.

With the downturn last week, the valuation gap has shrunk, but it remains elevated compared to its history. As of March 31, 2025, US equities had approximately 9 extra turns of valuation versus Global ex US equities; over the past 20 years the average valuation gap was ~4.68x.

If US equities were to return to their 20-year average they would decline another ~15-20% relative to their international peers (and that’s before any hit to corporate profits from the new tariffs impacting the “E” in the “P/E” ratio!).

LOOKING AHEAD (CONTINUED)

Longer Term:

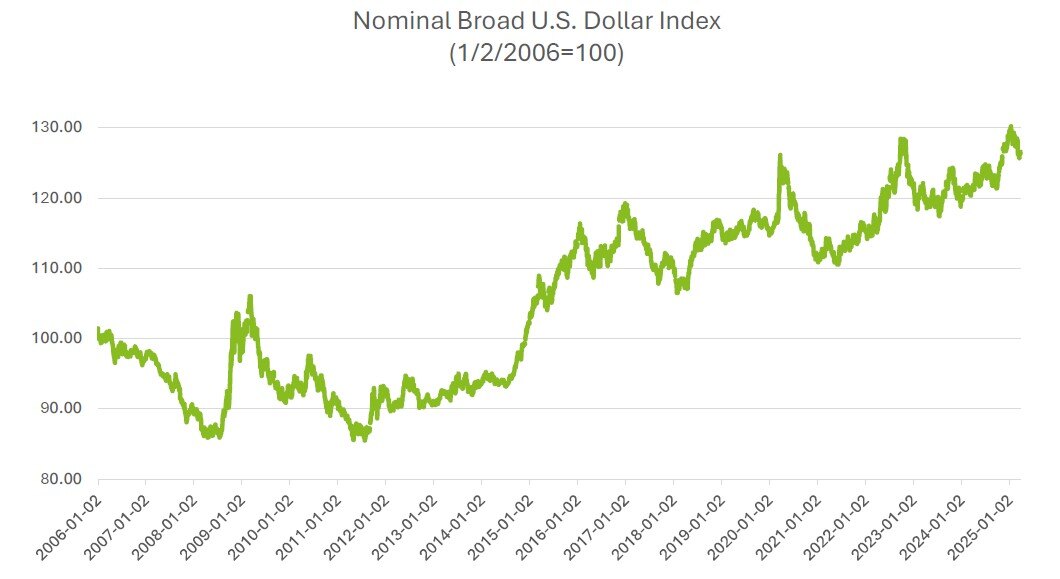

Watch the US Dollar.

The US dollar has been very strong in recent years. This has contributed to the strong relative performance of US dollar- denominated assets, as foreign investors have continued to sell their currencies to buy US dollar-based assets.

Nominal Broad U.S. Dollar Index (1/2/2006=100)

We think that the US dollar will likely remain the preeminent reserve currency for many years to come (at least), but there are real risks of the dollar weakening given the uncertainties, both economical and geopolitical, that the new tariff regime presents to global investors. The same foreign investors who have so willingly bought US equities and fixed income (including US Treasuries at staggering rates) may begin to diversify away from dollar-denominated assets. This could contribute to turning the rising US dollar tailwind into a falling dollar headwind.

Deglobalization will have real costs and impacts beyond the tariffs.

The COVID pandemic demonstrated the fragility of global supply chains, and it stalled the process of globalization in many ways. The new tariffs are a direct shot at what remains of globalization and the economic and financial institutions that support it. What comes after it is yet unknown, but with any sort of colossal shift in the economy there will be costs to be borne by many, with some bearing more than others. There is a risk that retaliation could expand beyond trade and tariffs.

Also worth noting – the process of globalization took many decades, and we expect the unwinding of deglobalization will take many years, at least. This is likely a paradigm shift that will take time to play out (factories can’t be built overnight!).

GOING FORWARD

Remain Diversified

Over the past year, we have encouraged clients to diversify portfolios that were especially heavy in US large caps (especially large cap growth) stocks into other asset classes, including international equities and investment-grade fixed income.

We continue to encourage clients to be properly diversified and allocated in accordance with their risk tolerance and investment objectives. If you have not already, work with your financial advisor to ensure that your portfolio is prudently diversified and invested.

Invest for the Long Term

It’s normal to watch the markets during periods of extreme volatility with concern. It’s not advisable to check your portfolio balances daily and panic.

There have been numerous events and shocks to the economy and markets over their history, and with enough time, markets have always rebounded. Drawdowns are normal, and they are part of the reason why equities return so much more than other asset classes over time. Stick to long-term investing for your goals.

Do Not Panic.

Some of the best days in the history of the US stock market occur after some of the worst days. Market drawdowns can sometimes provide investors opportunities to make thoughtful, prudent improvements to their portfolio, but its important to remain invested in accordance with your personal investment strategy.

If your investment horizon aligns with your liquidity needs, and if you are properly allocated and invested to meet your long-term goals, stick to your plan and ride out the storm. Working with your financial advisor can help provide more confidence with this planning.

The WIA Investment Team will continue to monitor policy, markets, and the economy, and provide you updates and our analysis in the weeks and months to come.

Sources:

- Morningstar Direct, “Rolling Returns”, accessed 5 April 2025.

- Douglas A Irwin, “Clashing Over Commerce: A History of US Trade Policy”, https://www.nber.org/books-and-chapters/clashing-over-commerce-history-us-trade-policy, accessed 5 April 2025.

- Tax Foundation, “Trump Tariffs: The Economic Impact of the Trump Trade War”; https://taxfoundation.org/research/all/federal/trump-tariffs-trade-war/; accessed 6 April 2025.

- Schneider, Howard. “Bessent’s Focus on 10-Year US Treasury Yield May Let Fed off the Hook | Reuters.” Reuters, 6 Feb. 2025, www.reuters.com/markets/us/bessents-focus-10-year-us-treasury-yield-may-let-fed-off-hook-2025-02-06/, accessed 6 April 2025.

- Powell, Jerome. Speech by Chair Powell on the Economic Outlook, Board of Governors of the Federal Reserve System, 4 Apr. 2025, www.federalreserve.gov/newsevents/speech/powell20250404a.htm, accessed 6 April 2025.

- Truth Social, Donald J Trump, https://truthsocial.com/@realDonaldTrump/posts/114280322706682564, accessed 6 April 2025.

- Bureau of Labor Statistics, “Employment Situation Summary”, 4 April 2025, https://www.bls.gov/news.release/empsit.nr0.htm, accessed 6 April 2025.

- Ice Data Indices, LLC, ICE BofA US High Yield Index Option-Adjusted Spread [BAMLH0A0HYM2], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/BAMLH0A0HYM2, 6 April 2025.

- Morningstar Direct, “Performance Reporting”, accessed 6 April 2025.

- Morningstar Direct, “Performance Reporting”, accessed 6 April 2025.

- Morningstar Direct, “Portfolio Characteristics”, accessed 6 April 2025.